The End of the App Grid

What replaces the home-screen grid of apps

The home-screen grid of discrete, tappable apps was an artifact of a specific cost structure — one that has quietly collapsed. When building software falls by an order of magnitude, the unit of software stops being the app.

For fifteen years the grid was the organizing metaphor of personal computing: a screen of icons, each a self-contained program you opened, used, and closed. That metaphor held because apps were expensive. Shipping a polished, production-grade application took a team, months, and a budget — so apps were few, deliberate, and worth a permanent place on your screen.

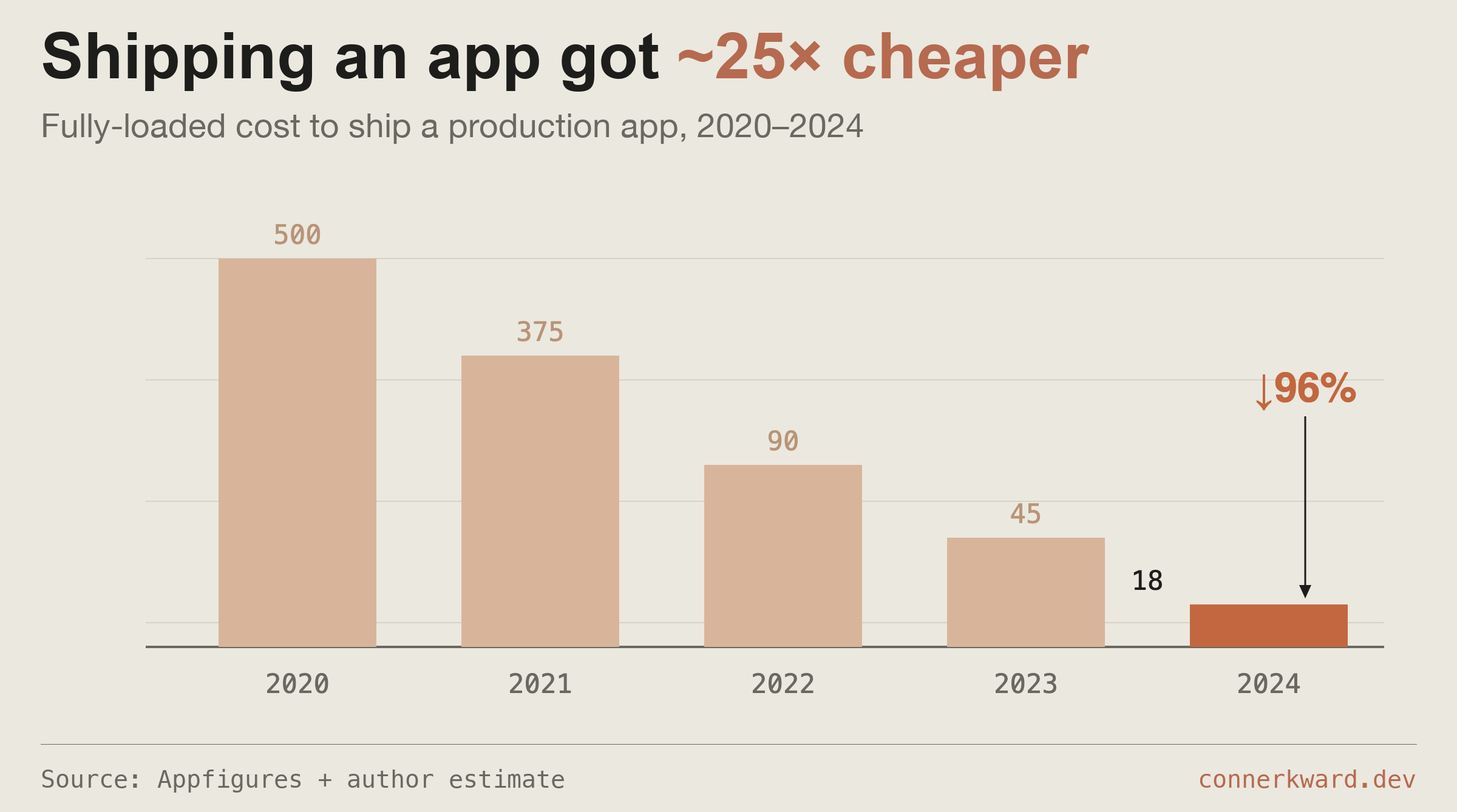

That premise is gone. The marginal cost of producing a working application has fallen roughly an order of magnitude in four years, and most of that drop has come since generative models made the expensive parts — interface, glue code, integration — close to free.

When the cost of a thing falls by 96%, you don't get the same number of them, cheaper — you get a different category of thing entirely. Software stops being something you install and becomes something that is summoned: generated on demand, used once, and discarded, the way you'd reach for a sentence rather than a saved document.

The capital markets saw it first

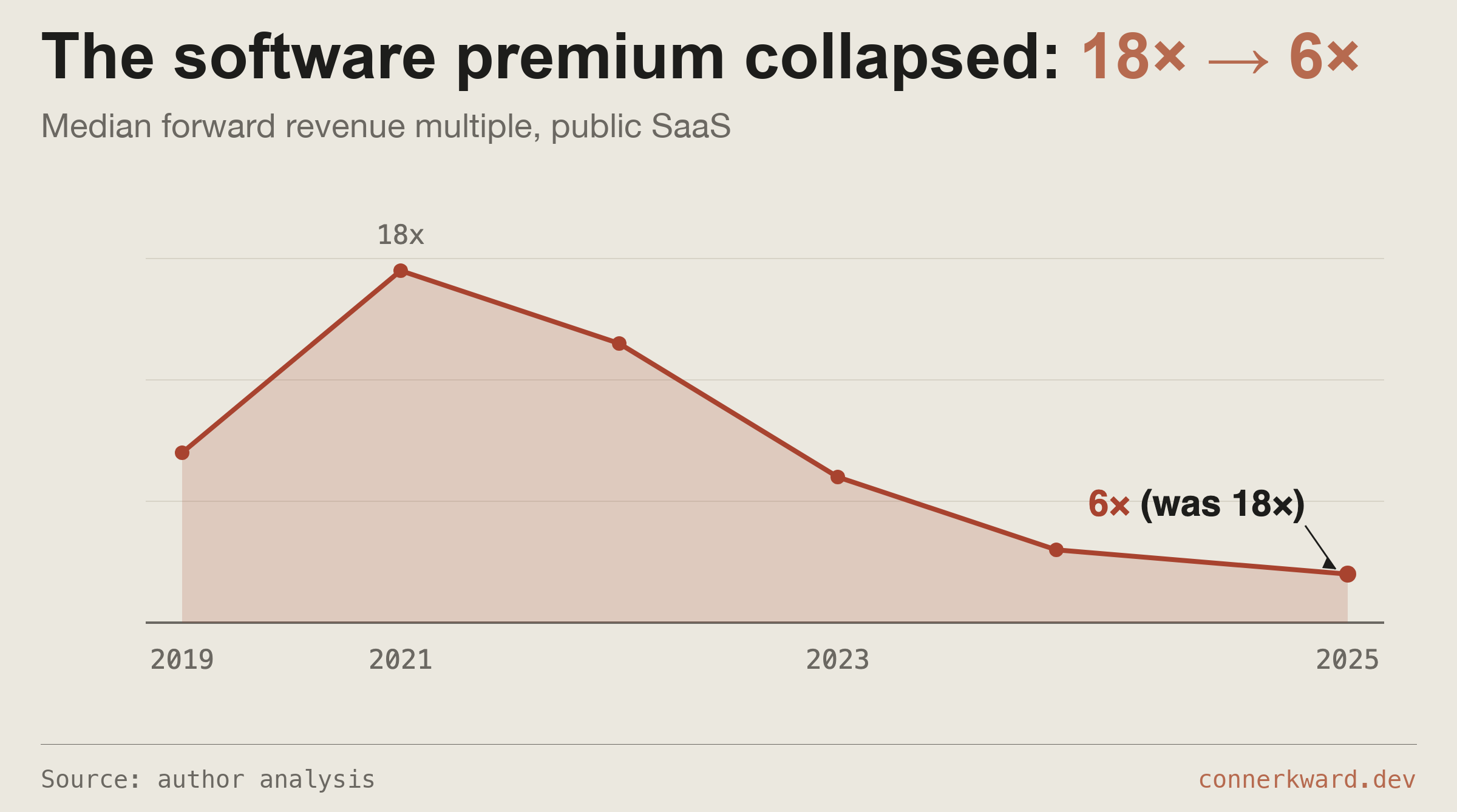

The clearest early signal wasn't in product — it was in price. The public software multiple, the number investors will pay per dollar of forward revenue, compressed hard off its 2021 peak, and it hasn't recovered the way previous drawdowns did.

Some of that is rates. But a structural read is harder to dismiss: if the moat of a SaaS company was the cost and difficulty of building the software in the first place, and that cost is collapsing, the durable advantage has to live somewhere else — in distribution, in proprietary data, in the workflow itself.

Where the grid breaks first

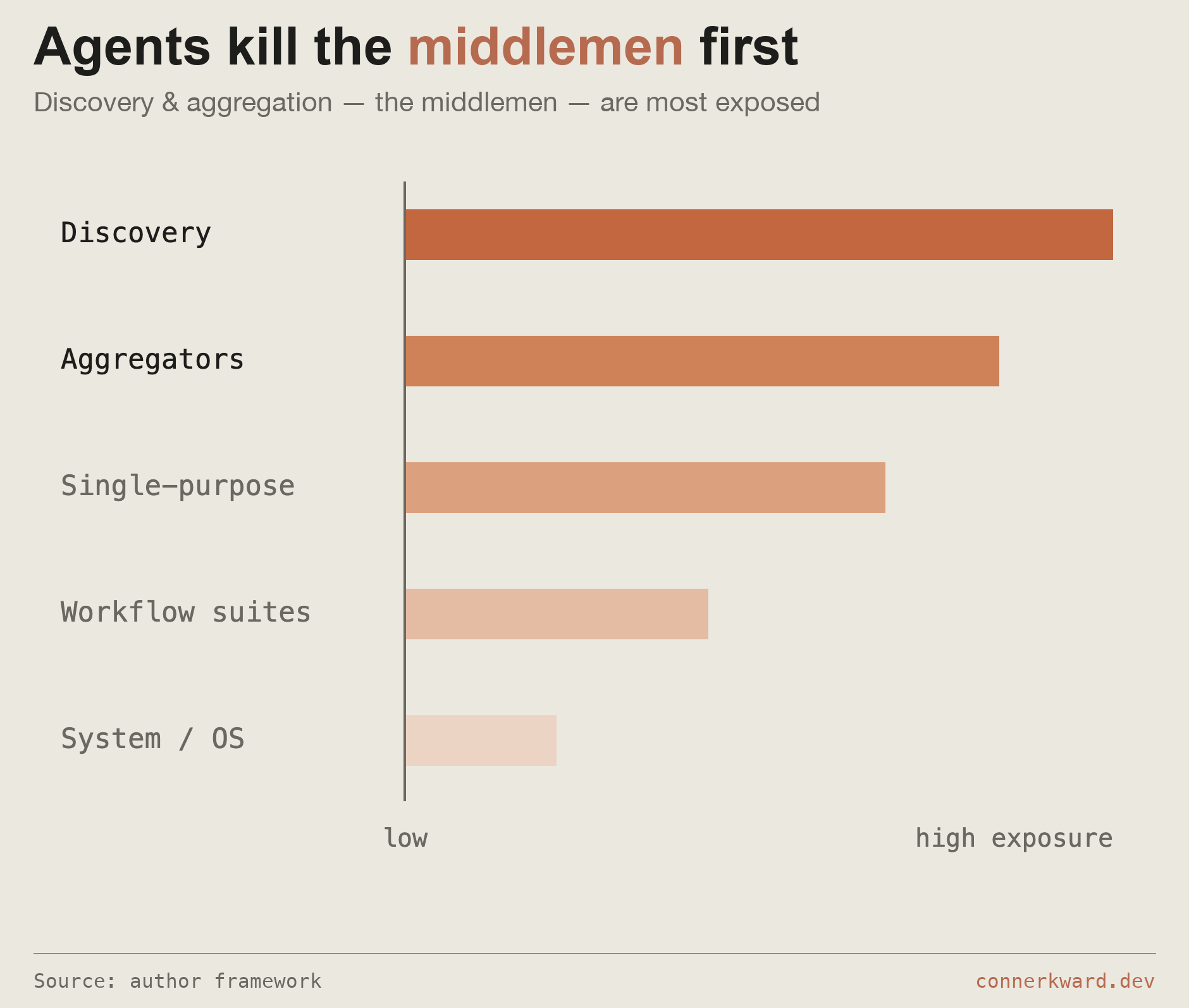

Disruption won't arrive evenly. The layers of the app economy most exposed are the ones whose entire value was finding and routing — the discovery surfaces and aggregators that sat between a user's intent and the thing that satisfied it. An agent that can act collapses that intermediary.

The defensible end of the spectrum is unglamorous: the system layer, the OS, the places that own the user relationship and the rails. The exposed end is exactly where the last decade's venture returns concentrated.

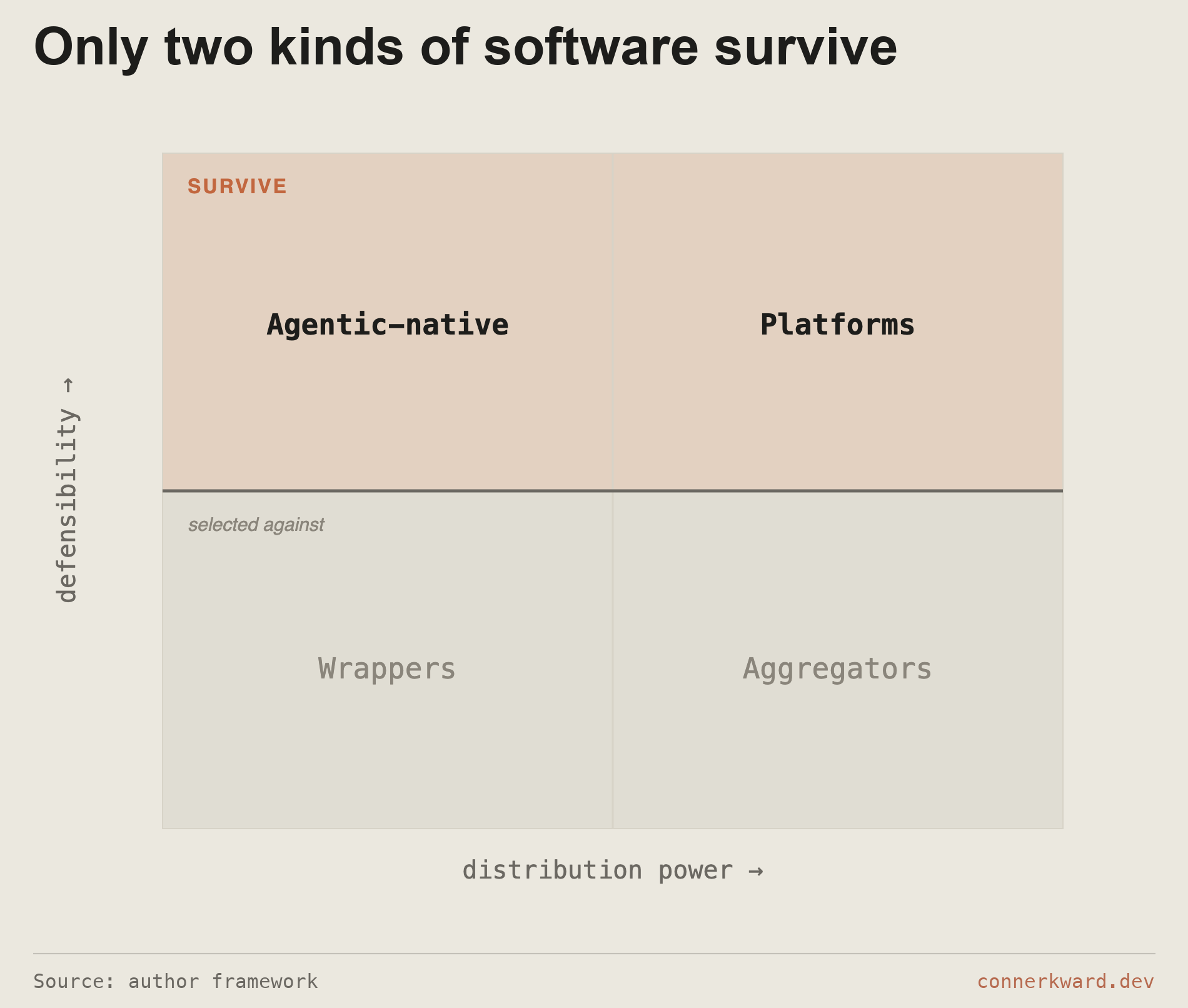

Who survives

Map the survivors on two axes — how much distribution power a firm holds, and how defensible its position is once software is cheap — and a rough typology falls out.

The incumbents survive on distribution they already own. The agentic-native firms survive by being built for the new cost structure from the start. The wrappers — thin layers over a model with no distribution and no moat — are the population the collapse selects against.

This is the first piece in a series; the next asks what luxury software looks like once function is free.